Understanding how do you pay back a reverse mortgage is critical for homeowners considering or currently holding a reverse mortgage. Unlike traditional mortgages, reverse mortgages allow seniors to access home equity without monthly payments, but repayment eventually becomes necessary. This article provides a comprehensive guide to repayment strategies, timelines, and considerations in 2026.

What Is a Reverse Mortgage?

A reverse mortgage is a special type of home loan available to homeowners aged 62 or older. It allows them to convert part of their home equity into cash without selling the home or making monthly payments. Lenders advance payments either as a lump sum, monthly installments, or a line of credit.

However, the question arises: how do you pay back a reverse mortgage? Unlike a traditional mortgage, repayment occurs under specific circumstances, such as when the homeowner moves out, sells the house, or passes away.

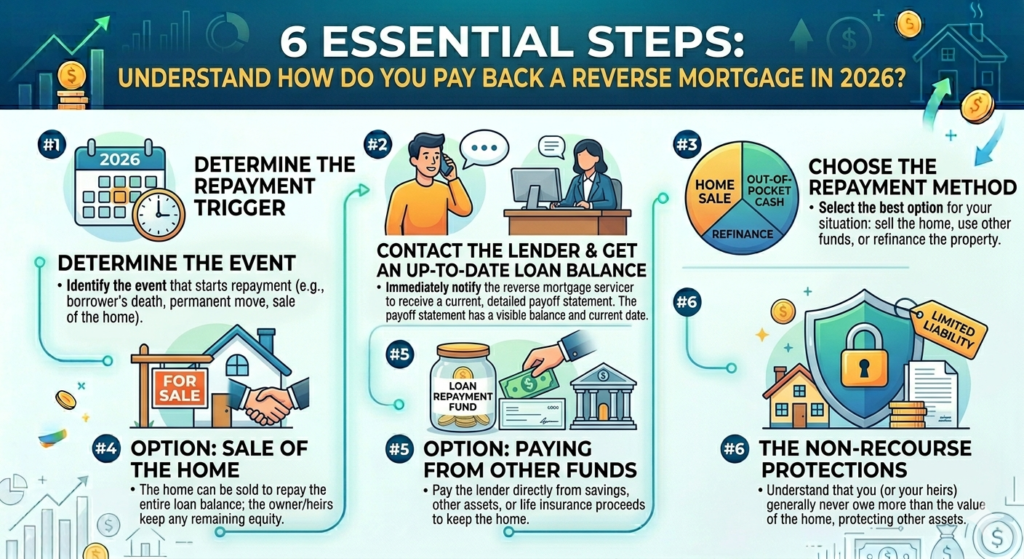

1. Understanding Repayment Triggers

Repayment of a reverse mortgage is not required until certain conditions are met. Key triggers include:

- Death of the homeowner – The loan becomes due and payable.

- Sale of the home – Any reverse mortgage must be paid off from the sale proceeds.

- Permanent move – If the homeowner permanently moves to assisted living or another residence.

- Failure to meet obligations – Failing to pay property taxes, insurance, or maintain the property can trigger repayment.

Knowing these triggers is essential to plan for how do you pay back a reverse mortgage.

2. Using the Home Sale to Repay the Loan

One of the most common ways to repay a reverse mortgage is by selling the home. The lender is repaid from the proceeds of the sale, and any remaining equity goes to the homeowner or heirs.

Example Table – Sale Proceeds vs Reverse Mortgage Balance

| Home Value | Reverse Mortgage Balance | Remaining Equity |

|---|---|---|

| $300,000 | $180,000 | $120,000 |

| $400,000 | $250,000 | $150,000 |

| $500,000 | $350,000 | $150,000 |

Selling the home is straightforward and ensures repayment without requiring cash from the homeowner or heirs, addressing one way to answer how do you pay back a reverse mortgage.

3. Repayment Through Refinancing or Traditional Mortgage

In some cases, homeowners or heirs choose to refinance the reverse mortgage into a traditional mortgage. This option allows borrowers to retain the home while establishing a structured monthly repayment plan.

Refinancing Table – Example Payment Scenarios

| New Mortgage Amount | Interest Rate | Term | Estimated Monthly Payment |

|---|---|---|---|

| $180,000 | 5.0% | 30 yrs | $966 |

| $250,000 | 5.5% | 30 yrs | $1,418 |

| $350,000 | 6.0% | 30 yrs | $2,100 |

This method is a viable answer for homeowners wondering how do you pay back a reverse mortgage without selling their property.

4. Repayment After the Homeowner’s Passing

If the homeowner passes away, heirs or the estate are responsible for repayment. Typically, lenders allow:

- Selling the home to cover the loan.

- Paying off the reverse mortgage from personal funds and retaining the property.

- Using a combination of sale proceeds and other estate assets.

Table – Estate Options for Repayment

| Option | Pros | Cons |

|---|---|---|

| Sell home | Loan fully repaid, heirs receive equity | Home no longer in family |

| Pay off with personal funds | Retain family home | Requires significant cash |

| Combination | Partial equity retained | Complex financial planning |

Understanding these options clarifies how do you pay back a reverse mortgage for families and estate planning.

5. Using Savings or Liquid Assets

Sometimes, homeowners or heirs use savings or liquid assets to pay back the reverse mortgage instead of selling the home. This approach avoids moving or selling valuable property but requires sufficient cash to cover the loan balance, including accrued interest.

Table – Cash Repayment Example

| Reverse Mortgage Balance | Interest Accrued | Total Cash Required |

|---|---|---|

| $180,000 | $20,000 | $200,000 |

| $250,000 | $35,000 | $285,000 |

| $350,000 | $50,000 | $400,000 |

This method is an alternative answer to the question: how do you pay back a reverse mortgage.

6. Considerations and Best Practices

Before deciding how do you pay back a reverse mortgage, homeowners should consider:

- Interest Accrual – Reverse mortgages accrue interest over time, increasing the repayment balance.

- Property Maintenance – Obligations to pay taxes, insurance, and upkeep remain.

- Loan Limits – Federal regulations cap how much can be borrowed.

- Consult Professionals – Financial advisors, estate planners, and HUD counselors can provide guidance.

Planning ahead can ensure repayment is manageable and equitable for heirs.

FAQs About Paying Back a Reverse Mortgage

Q1: When is a reverse mortgage due for repayment?

A1: Repayment is required when the homeowner dies, sells the home, or permanently moves out, or fails to meet obligations.

Q2: Can I pay back a reverse mortgage before it’s due?

A2: Yes, you can repay early using cash, refinancing, or other financial resources.

Q3: What happens if heirs can’t pay the reverse mortgage?

A3: The home is usually sold to repay the loan. Heirs are not personally liable beyond the home’s value.

Q4: Does paying back a reverse mortgage include interest?

A4: Yes, repayment includes the original loan plus accrued interest and any fees.

Q5: Are there options to keep the home while repaying?

A5: Yes, refinancing or taking a new mortgage can allow repayment while retaining ownership.

Conclusion

Understanding how do you pay back a reverse mortgage is crucial for homeowners, heirs, and estate planning. Repayment can be achieved through home sale, refinancing, cash repayment, or estate management. By considering triggers, planning strategies, and consulting professionals, seniors and families can navigate reverse mortgage repayment efficiently in 2026.